How much oil and gas could come from 'tiebacks'?

Summary

• The government is about to announce the details on how it will implement its manifesto promise not to issue new licences to explore for new offshore oil and gas fields.

• There have been reports that the government is considering exceptions to its licensing ban for discoveries that can be tied-back to existing infrastructure (so called “tie-backs”). The oil and gas industry claims that production involving tie-backs to existing infrastructure could unlock billions of barrels of oil and gas.

• However, according to new analysis from Uplift, tie-backs are likely to produce substantially less oil and gas than the industry claims.

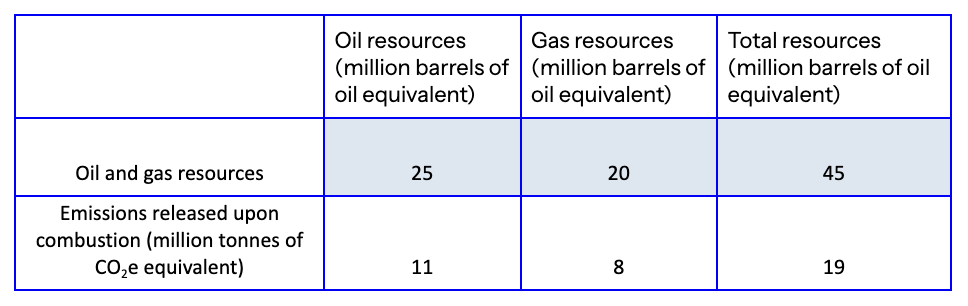

• The analysis in this report shows that new oil and gas discoveries within a 50km radius of existing production sites that would require a new licence to proceed contain just 25 million barrels of oil and 20 million barrels of oil (equivalent) of gas. This would be from five potential projects.

• The combined 45 million barrels of oil equivalent is the most that is commercially and technically recoverable at a sensible estimate of future oil prices. Whether any of these projects are given development consent - permission to actually produce oil and gas - is an open question and will be decided using new guidance requiring the government to take into account the total climate impact on any new production. For context, the Rosebank oil field would involve the extraction of nearly 500 million barrels of oil and gas-equivalent over the course of its lifetime.

Introduction

In their 2024 manifesto, the Labour Party set out that it will not issue any new oil and gas licenses to explore new fields. This was reiterated in the recent consultation on Building the North Sea’s Energy Future, which confirmed that the government “has been clear that it would not issue new licences to explore new fields”, while “not revoking existing licences and partnering with business and workers to manage our existing fields for the entirety of their lifespan”.

The oil and gas industry has repeatedly challenged the government’s plan to ban new licenses, claiming in the press that the North Sea could produce significant amounts of oil and gas with the right conditions. In particular, the industry claims that production tied back to existing oil and gas infrastructure could unlock billions of barrels of extra oil and gas. However, the industry’s claims are based on wildly optimistic assumptions about the investment climate which does not reflect the fact that the North Sea is a mature and expensive basin. Despite the fact that operators are already operating under a ‘maximum recovery of oil and gas’ regulatory regime, with generous tax breaks for new drilling, the North Sea is in steady decline.

New analysis from Uplift shows that new licenses tied back to existing infrastructure could unlock at most 45 million barrels of oil equivalent based on what is commercially and technically recoverable at a sensible estimate of future oil prices. This is a fraction of the amount that the industry claims is possible. The government’s likely licensing ban, even with a limited exception for production tied back to existing infrastructure, would be a world leading position and demonstrate a commitment to phasing out oil and gas production.

Tie-backs

A subsea tie-back connects offshore oil and gas fields to existing production facilities via pipelines and other infrastructure. To install tie-backs, a new well is drilled on the seabed, and equipment is installed that directly feeds into an existing field's production installation, much like a garden hose running from a tap to the garden, or, in this case, from a discovery well to a production facility.

Tie-backs can offer a cost-effective solution for continuing production at an existing facility without the upfront costs associated with developing completely new production equipment. Similarly, they can continue employment at a facility for a longer duration, as the production time of the facility is extended.

The distance a discovery can be tied back to a production facility isn't precisely characterised. Specific project characteristics can impact the feasibility of a tie-back distance, including water depth, existing production facility capabilities, and geology. Generally, at greater distances, power transmission becomes an issue. Some reports constrain deep-water tie-backs to 35km. Some facilities have managed tiebacks at distances over 100km.

Tie-backs analysis

Data from the North Sea Transition Authority (NSTA) has a total of 139 offshore discoveries. All NSTA discoveries (139), bar one, were within a tie-backable distance to a producing or close to producing fields*.

Forty-one discoveries are within current licenses. Ninety-eight discoveries are within relinquished licenses. No discoveries fall outside of current or relinquished licences.

Of the 98 discoveries that fall within a relinquished license, 97 discoveries are within 50km of a producing or close to producing field. A sensitivity analysis was conducted, where the size of the buffer was increased to 75km and reduced to 25km. No more discoveries (97) were pulled through by increasing the buffer size to 75km, and reducing the buffer to 25km pulled 92 discoveries through.

How much oil and gas could be produced from a licensing loophole?

The 97 discoveries within relinquished licenses (not within current active licenses) that are within a tie-backable distance to producing, or near-producing fields, were matched with reserves estimates. The discoveries that show resources higher than zero are deemed both economically and technically recoverable. Out of 57 matched discoveries, only five were deemed both economically and technically recoverable, with estimated resources greater than zero.

The total resources for oil and gas were estimated at 45 million barrels of oil equivalent, which represents resources that could be extracted under a licensing loophole. If burnt, 45 million barrels of oil would release approximately 19 million tonnes of CO2e.

Methods:

NSTA Shapefiles for offshore undeveloped discoveries, offshore fields, current and relinquished oil and gas licenses were mapped using QGIS (Geographic Information System). Oil and gas discoveries were filtered by a ~50km distance to currently producing fields, which additionally intersected with relinquished licenses but not current active licenses. The discovery data was then extracted from QGIS and matched with the Rsytad data for resources for discoveries. NSTA data and Rystad data were matched by discovery name and location.

Additionally, a sensitivity analysis was conducted, where the buffering distance was increased to ~75km and reduced to ~25km. Increasing the buffering distance to ~75km did not increase the number of discoveries, and reducing the buffering distance reduced the number of discoveries to 92.

59% of NSTA discoveries were matched with discoveries in the Rystad database. Discoveries that were in the NSTA data but not in the Rystad data (unmatched) are considered technically unrecoverable at the base case scenario. The ‘base case’ scenario reserves data has an oil price forecast that Rystad estimates from transaction markets. In the short and medium term, this is set by Rystad’s oil and market team based on the latest insight into the market liquid supply and demand balances. In the long term, the price is a weighted average of the implied oil price observed in the transaction market over the last six months. 9% of matched discoveries had resources greater than zero. Discoveries that show resources higher than zero are deemed both economically and technically recoverable.

The resources that could be extracted under a licensing loophole are the total resources from the matched dataset.

NSTA definition of discoveries: A discovery is a petroleum accumulation for which one or several exploratory wells have established through testing, sampling and/or logging the existence of a significant quantity of potentially moveable hydrocarbons.

Rystad's definition of discoveries: Discovery includes assets where discoveries have been made but are not yet in a phase of further development (appraisal, field evaluation).

*Producing, Production suspended - possible reserves remain, construction-FDP approved, Under appraisal - no FDP, Under appraisal future FDP.

Emissions calculations were conducted using DESNZ GHG Factors (2025).

All figures presented are rounded to the nearest whole number.